s. 44 of the SABS in the One-Two Punch Claim Handling Technique — Why I Believe Insurance Companies Do Not Pay

In Ontario, auto insurers use s. 44 of the Statutory Accident Benefits Schedule (SABS) as the legal basis for requiring the insured to attend an Insurer’s Examination(IE). It plays an integral part in handling insurance claims that make it difficult for injured victims to receive the benefits of their insurance policies.

Insurer’s Examination (IE) is a process during the claim handling where the insured is examined by another health practitioner who has no duty of care to the insured and is hired by the insurer.

Before I proceed, please know that I am not a lawyer. I cannot provide legal advice. And any of my words should not be taken as legal advice.

However, if you are paying for auto insurance like me, whether or not you have been entangled in legal proceedings, s. 44 seems a mystery — and I have questions I will be sharing. Please read along, pause, then consider whether you should have questions too.

One-Two Punch Claim Handling Technique

It is carried out by denying the insured payment or benefit (first punch), immediately followed by requiring the insured to attend an IE (second punch).

But wait, SABS stipulates strict requirements. SABS is the regulation under the Insurance Act about our entitlements to the auto insurance policies we are mandated by the government to pay.

What Does SABS Say When an Insurer Denies or Refuses Payments or Benefits?

When giving notices of denials of benefits, depending on the type of benefit, there is a timeline restriction, typically within ten business days after the insurer receives the claim. And the medical and any other reasons for its denial, among other things, should be given. See subsections 36(4)(7), 37(4)(6), 38(8)(14), 42(3)(13), 43(2) and 45(3)(5) of the SABS.

The timeline requirement — sounds like it is straightforward. But sometimes it is not. If the insurer sent it by regular mail, how do you calculate the ten business days? Subsection 64(2) will help you. And, if for an unusual reason, you did not receive the letter, ask or find out whether your insurer informed you beforehand that you should expect to receive a response to your claim within ten business days — it is the regulation.

The medical and any other reasons — what does it mean? With this, the Licence Appeal Tribunal (LAT) provides some assistance. At the very least, it should include specific details about the insured’s medical condition. It should be clear and sufficient enough to allow an unsophisticated person to make an informed decision to either accept or dispute the insurer’s decision — requiring the insured to attend an IE (M.B. v. Aviva Insurance Canada, 2017 CanLII 87160 (ON LAT)). It is contextual and turns on the unique facts in each case.

What Does SABS Say When an Insurer Requires IE Attendance?

Subsection 44(1) dictates that an Insurer’s Examination (IE) should not be required more often than is reasonable and necessary. Subsection 44(5)(a) stipulates that if the insurer requires IE attendance, it should give the insured person (claimant) notice about the medical and any other reasons for the examination, among other things. The regulation strictly requires that the insurer give its medical and any other reasons. Otherwise, the insurer is not performing its obligation according to the law.

What seems to be the problem?

First, insurers provide medical and any other reasons that are vague and from boilerplates, such as “the patient does not appear to show objective signs of improvement despite continuing treatment” or “the frequency of care does not generally diminish over time”. Go on and search the quoted phrases in CanLII. A longer list of boilerplate reasons is a discussion for another time.

Second, denial of payment or benefit and requiring attendance to the Insurer’s Examination (IE) happen in quick succession (one-two punch). There is not enough time to settle the dispute on a denial of payment or benefit based on insufficient or deficient notice before the required Insurer’s Examination could be disputed, also on the same basis.

It is interesting that regardless of the insured notifying the insurer about the non-compliance of its notice obligations, the insurer is firm on its one-two punch. It leaves the insured with only two options: bring the dispute to the LAT or give up entitlements to insurance benefits. The lamentation you hear more often is that “insurance companies do not pay”.

Also, insurers often stipulate in the notice of IE attendance that the insured cannot apply to the LAT until the insured attends the IE. And this, regardless the insured disagrees with the IE attendance, at times, leads to the insured attending the IE unwillingly. And this is used against the insured at the LAT.

The Dispute at Licence Appeal Tribunal (LAT)

At the LAT, it starts with the burden on the insured to prove the claim is reasonable and necessary. It puts considerable weight on the insured from the start. In my opinion, it contradicts the policy objective of the legislation that accident victims promptly receive the statutory accident benefits to which they are entitled under the Act and their automobile insurance policies (Monks v. ING Insurance Company of Canada, 2008 ONCA 269 (CanLII)).

QUESTION: Why should the review of whether the claim is reasonable and necessary come ahead of reviewing whether the insurer’s notice of denial is not compliant with the strict requirements in the SABS?

Inconsistencies in LAT’s Review of Insurer’s Notices of Denials

At the LAT, reviewing the insurer’s notice of denial that forced the insured into a legal dispute is not mandatory. And when it is brought up, the analysis and the outcome are inconsistent.

QUESTION: Why is the review of the insurer’s notice not mandatory when the insurer’s notice obligation is stipulated in the legislation (ss. 36(4)(7), 37(4)(6), 38(8)(14), 42(3)(13), 43(2) and 45(3)(5)of the SABS)?

Inconsistencies in LAT’s Review of Insurer’s IE Notice (s. 44)

Similarly, the review of the Insurer’s Examination (IE) notices is also inconsistent. And at times, it is absent.

QUESTION: Why is the review of the insurer’s IE notice not mandatory when the insurer’s notice obligation is stipulated in the legislation, s. 44 of the SABS?

And when the insurer’s IE notice is reviewed, the analysis and the outcome often favour the insurer. The LAT declares that insurers are not held to a high standard of perfection in claim handling processes. Meanwhile, it is put upon the insured, who has no control or knowledge of the intricacies of the claim-handling process, to point out the mistake and give allowances for insurers to correct it (see Noor v Intact Insurance Company, 2022 CanLII 53732 (ON LAT)).

In cases where the insured did not attend the IE, the insured usually loses the claim.

In cases where the insured attended the IE despite issues with the insurer’s IE notice, the insurer argues that there is no issue in its IE notice because the insured complied with IE attendance. And the insurer likely wins the argument.

IE Examiner, Insurer’s Expert Witness

S. 44 holds that a health practitioner or someone with expertise in vocational rehabilitation may conduct the Insurer’s Examination (IE). For this discussion, I will refer to it as IE examiner.

In the courts, it is established that an IE examiner is considered an expert witness. And as I mentioned earlier, the IE examiner is hired by the insurer and has no duty of care to the insured. The IE examiner is for the insurer’s defence in a legal dispute.

Note that an IE is set up during the claim handling when the insurer contemplates denying the insured payments or benefits. The insurer has prepared its expert witness even before the insured has decided to apply to the LAT. Unless someone has first-hand experience in the LAT or the courts, the insured is never informed that the IE is the insurer’s preparation for an anticipated legal dispute.

It seems insurers use s. 44 to set up their defence before a legal matter starts, during the handling of the claim, because they intend to deny the insured payment or benefit. It is my observation.

QUESTIONS:

Should it be acceptable and procedurally fair for insurers to set up their expert witness and litigation defence during the claim handling process before a legal dispute starts?

Should the insured be informed about it as a right under the insurance contract (policy)?

The LAT’s Reliance on Insurer’s IE examiners/Expert Witnesses

Several cases adjudicated in the LAT relied on the insurer’s IE examiners or their reports, even when the examination of the insurer’s IE notice was absent. I am not a lawyer. But I believe that the principle in our justice system is that a party should not be allowed to use evidence that is not vetted to have been properly acquired by the party who wants to use it.

QUESTION: Should it be acceptable and procedurally fair for the LAT to rely on insurer’s IE examiners or report without correctly examining the sufficiency of the insurer’s IE notice under s. 44 of the SABS?

Powerful Tool — s. 44 in One-Two Punch

Insurers are organizations already a force to reckon with by the insured. And the questions concerning the adjudication landscape in the LAT and the insurers’ One-Two Punch Claim Handling Technique creates a significant imbalance where the insured victims are at the losing end.

One-Two Punch Technique Equates with Insurer’s Economic Gain

I don’t think I have to convince anyone that insurance companies make money. I like to share my observation of the relation of the One-Two Punch Claim Handling Technique with the economic gain by the savings of not spending the money towards the insured persons’ benefit entitlements — not paying or avoiding payments to the insured victims of car accidents.

Health Claims Database

Note: The HCDB Standard Report version, the basis for the figures in this article, is no longer available on the IBC website. However, the version available portrays an identical message context.

The Insurance Bureau of Canada (IBC) published a report on claims development of victims of car accidents in 2013 (Health Claims Database-HCDB Standard Report, September 2022). You’re curious why 2013? IBC does not have enough data about the development of claims after 2013. The natural progression between the date of the accident, the claim for benefits, the insurer’s handling or payments and the victim’s recovery based on the severity of the injury are the reason for not having enough data. It is explained in more detail in the IBC report.

What caught my attention was the insurers’ spending on IEs compared with the medical and rehabilitation expenses they paid to the victims.

627 claimants did not receive payments, but $1,929,450 was spent on IEs — an average of $3K per accident victim.

35,997 claimants received an average of $ 2,058.13 each for injuries determined by the insurers as “minor”, where entitlement is capped at $3,500. The average IE spent per claimant is $751.48, more than one-third of the benefits paid to the victim.

22,554 claimants were approved with entitlement to the regulated maximum of $50K. An average of $ 9,985.21 per claimant was paid. The average IE spent per claimant is $5,236.63, more than half of the benefits paid to the victims.

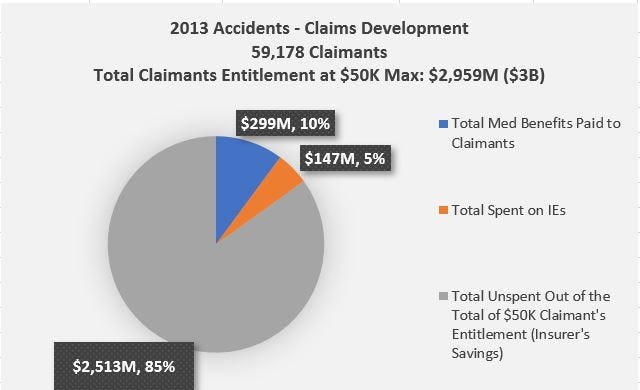

What does the picture look like for the whole industry?

The insurance industry spent $147M on IEs, almost half of the $299M paid to the victims — gained savings of around $2,513M (approximately $2.5B) out of the total regulated maximum entitlement of $2,959M ($3B) in medical benefits for the 59,178 insured victims of accidents in 2013.

QUESTIONS: Do you agree with these observations? Do you find it outrageous? And should this be a concern?

Continuing Dilemma of the Insured Victims of Car Accidents — What Now?

We do not have the claims development picture for accidents after 2013. The empirical evidence is not yet available to show whether the image is more dismal. But there is a consensus that the vulnerable victims of car accidents are kept in the losing lane.

If you are someone or know someone on this road facing insurers’ denials of benefits, financial constraints and other things, you may have asked yourself, or you have to ask yourself, whether the uphill battle is worth it and whether your spirit has the strength to go through it. There is no absolute wrong or correct answer. There is no judgment whether you choose not to go through it or quit midway.

However, if you have questions in the same vein as I laid out here and you have a vested interest, the spirits and the guts to forge ahead, I wish you strength. I hope you will keep on reading. Can we invoke the laws? Should we ask for them to be upheld?

How to leverage the current statutes or legislation?

Here are my opinions….

The legislation provides the framework aligned with the policy objective that accident victims promptly receive the statutory accident benefits to which they are entitled under the Act and their automobile insurance policies.

The adjudication of the disputes arising from the insurers’ notice of denials leaves much to be desired. The questions and ambiguities on the correct application of the laws under the Insurance Act and respective regulations nurture the environment of significant disparity between insurers against the insured, to whom insurers have a duty of care.

If you are still reading this, I am here to share the experience of someone’s plight that is now before the Supreme Court of Canada, waiting for its decision on whether the questions on issues of law about the insurers’ notice obligations and procedural fairness rendered by the LAT or our courts have public importance (Silverio Pereira v. Aviva General Insurance Company).

Questions in Issue in the Memorandum submitted to the SCC

1. Should insurers be permitted to issue insufficient notices of denial of insurance benefits or payments and not be obligated to pay the insured without examining the insurer’s duty to give notice as per SABS?

2. Are procedural decisions that deprive an insured (party in the dispute) the opportunity to present his case fully and fairly under the umbrella of the Tribunal being the master of its own house or procedures and be owed deference in the appeal of its decision?

Whether or not the highest court of our land decides the public importance of the questions in issues, your opinion weighs heavily and carries more substance.

In my opinion, we should keep urging and forging ahead for the correct application of the legislation. It is on the side of the public citizens, including s. 44. Although, based on the One-Two Punch Claim Handling Technique, my opinion is that insurers should not have the right to an IE during the claim handling process. For now, I will stop here before going down the rabbit hole. I reserve this discussion for another day.

I hope the questions I raised resonate with you. And with these questions, I hope it encourages you to seek resolutions leveraging the provisions of the statutes in place to provide the insured with the peace of mind duly expected from the insurance contract (Whiten v. Pilot Insurance Co., 2002 SCC 18 (CanLII), [2002] 1 SCR 5955).

As a final question, do you find the disparity between the insurance industry spending on the Insurer’s Examinations and benefit payments to the insured a huge concern?

Author’s Notes:

- The Health Claims Database-HCDB Standard Report used as the statistical data source and basis in this article is no longer available on the IBC website. However, the recent HCDB Standard Reports still present the same observations and issues discussed here.

- Any comment or question outside the scope of the content subject matter, please send them by clicking here. We will address your question through that forum.

Leave a Reply