NOTE: The following is a submission responding to the Financial Services Regulatory Authority of Ontario’s (FSRA) invitation to comment on Ontario’s Auto Reforms Initiative.

Author: Ninette Ibanez

Comments Submission: FSRA’s Consultation on Auto Reforms

Establish as a Priority: Set transparent, meaningful (relatable) and objective measurements of a consumer outcome of fairness and the government’s consumer protection mandate

“Consumers injured in auto accidents receive the care they need” is a consumer-friendly and all‑encompassing definition of consumer outcome expected by Ontarians when they follow the mandate of purchasing their auto insurance policies.

As a general observation, the scope of FSRA’s consultation papers is focused only on the health practitioners’ business administration/operations, creating cost burdens and resource challenges diverting from the appropriate care to injured accident consumers and reducing the pool size of available healthcare practitioners because the administrative burdens are disincentives.

Issues

The contentious issue is that Ontarians who experience going through the claim process to get the care they need for their injuries from auto accidents are not receiving the necessary care.

1. There is no report or study objectively showing that consumers injured from auto accidents were able to recover and return to their work and normal life before the accident. There is no known initiative to investigate this matter.

2. Even though some data is available, there is no known initiative reconciling the information from multiple sources with the consumer outcome to objectively explain whether the consumers injured in auto accidents are substantively receiving the care they need.

(i) The Tribunals Ontario reported the LAT-AABS received 13,983[1] appeals in 2022‑23. The Ontario Trial Lawyer’s Association (OTLA), in their article[2] calling for an immediate review of the LAT, expressed the disturbing trends at the LAT, where claimants dispute their insurers’ refusals to pay their insurance benefits. Quoted from the OTLA:

- “LAT adjudicators have ruled in favor of insurance companies more than four times more often than they have for self-represented individuals.”

- “The LAT has issued nearly 4,500 decisions…only 217 decisions have involved self-represented individuals.”

- “…out of the 4,500 decisions made by the LAT, self-represented individuals have succeeded only 33 times”

- “In 2017, the success rate for applicants stood at 33%. However, by 2023, this figure had dramatically declined to just 10%.”

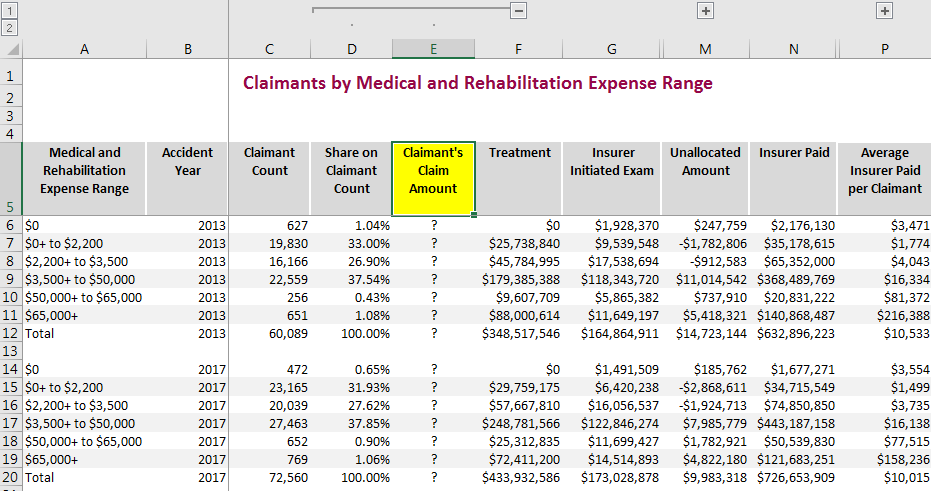

(ii) The HCDB Standard Report 2024H1 (HCDB Report) leaves much to be desired. However, it reported 56,263 auto insurance claims in 2022, where the insurer spent an average of $7,473 per claimant (Insurer Paid). The Insurer Paid include the insurer spent on their agents preparing the Insurer Initiated Examination (IIE)[3] reports used to refuse payments of medical treatments and as “expert witness” reports in the anticipated dispute litigations at the LAT. It means that the relevant spending that went towards the claimant’s medical treatments was even less than $7K.

The HCDB Report tables do not include the breakdown of the Insurer Paid between the spending towards claimant’s medical treatments and the IIE for refusing claims, except for the table Claimants by Medical and Rehabilitation Expense Range[4], reporting only the years 2013 and 2017. For illustration purposes, the percent of total IIE over total Insurer Paid in 2017 is around 24%. Applying it to the 2022 Insurer Paid average, the truthful figure for the average spent towards medical treatments was $5,679.

The HCDB Report does not disclose the Claimant’s Claim Amount submitted to the insurers, concealing the variance between the submitted claim amounts and the insurer paid towards the claimant’s medical treatments, which s relevant in determining consumer outcome.

Figure 1: Source: Insurance Bureau of Canada, 2024 Ontario Health Claims Database (HCDB) Standard Report[5]

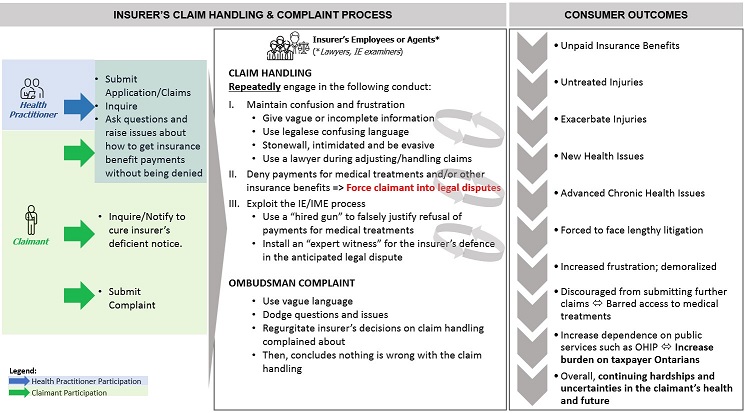

3. The claim handling process is complex. Claimants have no adequate information and assistance to navigate the insurer’s claim handling process so that the insurer would pay the benefit claims necessary to get the care they need. Instead, claimants face denials of benefit payments and lengthy and unsuccessful litigations, resulting in undesirable consumer outcomes.

Figure 2 – Landscape of the Auto Insurance Claim Handling – Consumer Experience

Icons made by authors from www.flaticon.com (Freepik, howcolour, juicy_fish, shmai)

The state of the claim handling landscape does not reconcile with the sought-out consumer outcome that those injured in auto accidents receive the care they need. Although sources of information are disparate and the reported data has gaps (missing relevant data points), they raise a red flag, exposing a real issue: The enormous barriers to consumers’ access to their insurance benefits.

Recommendations

A. Enhance the HCDB Report.

Ensure transparency between the amount spent on the claimants getting their medical treatments and the insurer’s expenses on activities towards not paying the claims, such as the cost of IIEs.

(i) Add the following data to every report table/worksheet:

- Actual or Submitted Claim Amount,

- Insurer-Denied-Amount[6],

- other category of insurer’s claim spending outside the coverage (e.g. legal expense), and

- duration between claim submission and insurer approval/denial.

(ii) Add the capability to drill down to the insurer in every report table/worksheet or provide the report tables/worksheets broken down per insurer.

(ii) Add the Claimants by Medical and Rehabilitation Expense Range table for all the accident years, not just 2013 and 2017.

B. Enhance the HCAI System.

(i) Allow claimants to access the HCAI System

(ii) Publish APIs[7]. Architect/design the system to be agile and optimized for third-party integrations.

(iii) Seek consumer participation in the business requirements (from consumer panel or consumer advocate communities)

C. Tackle the barrier to consumers’ access to the insurance benefits

(i) Carry out an in-depth and industry-wide investigation of adjuster’s claim handling treatments of claimants

(ii) Implement a pro-active and regular review (audit) of the claim handling process that is reported to the public domain

(iii) Consider or evaluate transferring the claim handling process from the insurers to a neutral body. And/or impose licencing on the claim adjusters, including the insurer’s employees.

(iv) As per s. 268.3(1) of the Insurance Act, FSRA to develop guidelines for consumers and insurers alike in interpreting and the operation of the SABS, especially in the following areas:

- Unambiguous criteria using plain language on the meaning of “medical and any other reasons” copiously used by insurers (i) to deny claims or (ii) to irrationally subject the claimant to an Insurer’s Examination to go against, indirectly smearing the claimant’s health practitioner’s diagnosis and recommendation to their patient to recover from the auto accident.

- Clarify section 64(1) of the SABS, specifically, whether the insurer should not be allowed not to notify the consumer of its preference or changing preference between sections 38 and 39.

- Continuous development of guidelines based on the results of the audit/review of the claim handling process.

- Intertwine the guidelines with the UDAP Rules.

D. Review the objectives of the Insurer’s Examination[8] balancing with the consumer outcome.

Insurers copiously utilize the Insurer’s Examination as the utility and means for refusing payments for the claimant’s (injured individual’s) medical treatments and forcing the claimant to pursue litigation where the trend shows claimants’ success is at a significantly low and declining rate. It is not an acceptable consumer outcome and requires immediate action to fix the issue.

In the interim, FSRA should establish guidelines on the interpretation and operation of the insurer’s utility under section 44 of the SABS, adhering to the consumer-centric purpose of the legislation and framed within the UDAP Rules.

E. Review the Minor Injury Guideline.

The Minor Injury Guideline (MIG) with the monetary limit associated with it (MIG Cap) creates a landscape where consumers injured from an auto accident who were unable to recover and get back to their normal life and still require medical treatments corresponding to those defined in the MIG but had exhausted the MIG Cap are without assistance. Insurers keep these consumers stuck at the MIG Cap without considering the injured person had not recovered to the state before the auto accident.

I recommend the options below:

- Institute the MIG Cap as the monetary limit only for not requiring the insurer’s approval and remove the type of medical treatment (classification under the MIG) as criteria for refusing to pay the medical treatment.

- Increase the MIG Cap in Ontario as offered by the community of health practitioners.

F. Review the language.

- Relabel “non-catastrophic injuries” with “non-minor injuries” when describing and referring to the scope of the monetary limit set in section 18(3)(a) of the SABS. Labelling injuries as non‑catastrophic dilutes the severe effects of the non-minor injuries affecting the lives of consumers injured in auto accidents. It flows into the insensitive demeanour of handling claims as administrative paper shuffling.

- The Claim Amount, the figure entered in the OCF forms submitted to the insurers for payments, should not transition to any other label as shown in the HCAI system referring to said figure as “proposed” or “estimate”. The inaccurate labelling of the Claim Amount could be why the HDCDB Standard Report does not report it. It contributes to a misguided theory that consumers injured in auto accidents receive the care they need based only on the insurers’ spending (Insurer Paid). The misguided theory accepted as the status quo further conceals the unfairness to vulnerable consumers suffering from the effects of auto accidents.

G. Review the objectives of setting a cap on the insurer’s liability to pay at the transaction/per medical treatment level

Consistent with my general observation on the scope of FSRA’s consultation papers focused only on the health practitioners’ business administration/operations, there is no real benefit to the consumer regulating the per unit medical treatment rate of the health practitioner selected by the consumer.

It is more helpful to inform the consumers of the industry-standard rates and ultimately let them choose the healthcare provider/practitioner they deem will provide the care they need to recover (consumer’s choice).

Unless there is sufficient and objective evidence of prevalent and industry-wide price gouging from the healthcare providers, the regulatory efforts focused on burdens on health practitioners’ business administration/operations are disincentives, reducing the pool of health services available to the consumers injured from auto accidents.

[1] Tribunals Ontario, 2022-23 Annual Report, Table 2: LAT-AABS Caseload Overview, Appeals Received in 2022-23

[2] November 4, 2024, Ontario Trial Lawyers call for immediate review of the Licence Appeal Tribunal, online: https://www.otla.com/docDownload/2502204

[3] Ontario Health Claims Database HCDB Standard Report – 2024H1 (July 2024),Insurance Bureau of Canada, online: https://a-us.storyblok.com/f/1003207/x/39162399ea/hcdb-standard-report-2024h1.pdf, p. 62 (PDF p. 63)

[4] IIE is also called IE (Insurer’s Examination) or IME (Insurer’s MedicalExamination)

[5] Filename: Ontario Health Claims Database HCDB Standard Report – 2024H1 Data File (.xlsx), Tab “expense range”, online: https://www.ibc.ca/industry-resources/insurance-data-tools/health-claims-database-hcdb

[6]The figure can be derived if the report includes the Actual or Submitted Claim Amount.

[7] Acronym/Technical reference to Application Programming Interfaces

[8] Interchangeable with Insurer’s Initiated Examination (IE) or Insurer’s Medical Examination (IME)

Leave a Reply